Accounts, records and audit under gst

Accounts, Records and Audit under GST

GST law has been a major indirect tax reform implemented in India. With the intention of a strong and transparent tax governance system, GST Audit has been implemented under the law which is applicable to tax payers operating over a prescribed limit.

Since GST Audit has been implemented for the first time, it is very important for a taxpayer as well as an Auditor to shift their focus to the nuances and technicalities of Audits under GST.

Regulation under GST law for Records and Audit.

According to Section 35 of CGST Act, every registered person shall keep and maintain all records at his principal place of business. Principal place of business is the place which is mentioned in the certificate of registration. Where more than one place of business specified in certificate of registration, accounts and records of each place of business shall be maintained at such additional place of business.

Section 35 also says, every registered person whose turnover during a financial year exceeds the prescribed limit (which is 2 Crores at present) shall get his accounts audited by a Practicing cost accountant (CMA) or a Practicing chartered accountant (CA) and shall submit a copy of the audited annual accounts, the reconciliation statement duly certified, in FORM GSTR-9C.

The accounts and records are specified in rule 56 of GST Act

Rule 56 says: Accounts and Records shall be maintained separately for each activity namely

v manufacturing

v trading and

v provision of services

List of records suggested under GST law

Inward Supply Records:

This is also records for input tax credit. Inward supply records include:

·Raw material purchase register:–– Raw material register should be recorded item wise. Records for imported and domestic items should be recorded separately. Suggested to contain the following:

v Item’s name

v HSN code

v GSTIN and name of supplier

v applicable GST rate,

v taxable value and tax amount

v status whether purchases are from registered or unregistered dealers

·Traded goods purchase register:–– Traded goods register should be recorded item wise. Records for imported and domestic items should be recorded separately. Suggested to contain the following:

v Item’s name

v HSN code

v GSTIN and name of supplier

v applicable GST rate,

v taxable value and tax amount

v status whether purchases are from registered or unregistered dealers

·Register for services received:–– Register for services received should be maintained separately for each service. Records for imported and domestic services should be recorded separately. Suggested to contain the following:

v Nature of service received

v GSTIN and name of supplier

v applicable GST rate,

v taxable value and tax amount

v status whether services received from registered or unregistered dealers

v status whether reverse charge is applicable

v status whether ITC is claimed in 3B or not

·Register for purchase of consumables:–– Consumable goods register should be recorded item wise. Records for imported and domestic items of consumable goods should be recorded separately. Suggested to contain the following:

v Item’s name

v HSN code

v GSTIN and name of supplier

v applicable GST rate,

v taxable value and tax amount

v status whether purchases are from registered or unregistered dealers

v status whether ITC is claimed in 3B or not

·Register for Credit Notes and Debit Notes issued by vendors

·Register for Purchase of Capital Goods

Procedure of Audit of Inward Supplies

To conduct GST Audit of Inward Supply, an auditor has to

Verify register of inward supplies item/service-wise to ensure eligibility or in-eligibility of ITC. Verify whether any inward supply is under reverse charge. If so, verify whether tax liability of reverse charge has been paid through cash ledger as liability of GST under reverse charge can only be paid through cash ledger.

Verify such register with purchase invoices of suppliers. Determine whether purchase invoices of all such suppliers have been prepared in accordance with GST Law mentioning GSTN number of business.

Verify whether pro-rata credit is taken in case of short receipt or partial quantity rejection as ITC is not available on material rejected, destroyed or short received.

Register of inward supplies should contain supplier’s name, supplier’s GSTIN, Invoice No. & date, items Name, items HSN code, GST rate, taxable amount and tax Amount.

Verify lists or credit notes received from vendors to reverse ITC claimed.

Verify reversal of Input Tax Credit if supplier has not been paid within 180 days from issue of invoice date as per rule 37. Aging report of vendors may be verified to check compliance.

Verify reversal of ITC as per Rule 39 - reduction in ISD credit on receipt of credit note from ISD distributor

Check reversal of ITC as per Rule 42 - reversal of ITC on input goods or services purchased due to making exempted supplies or not using for business purposes. Check Receipt of these goods or services & ITC Status.

Verify reversal of ITC as per Rule 43 - reversal of ITC on capital goods due to making exempted supplies or not using for business purposes. Verify receipt of these capital goods ITC Status.

Tax payers have to keep records of input used in supply for such goods or services as input tax credit is not available on supply of exempted goods or services***. Where input Tax credit is not identifiable to individual exempted goods or service then total value will be pro-rated for disallowance of Input Tax Credit e.g. input tax credit of capital goods producing both exempted and taxable goods may not be identifiable to individual production of exempted goods or taxable goods etc.

Already mechanism to reverse input tax credit is available under ITC rule

Verify whether ITC under goods or services mentioned under section 17 (5) (blocked credit) has not been availed. E.g. Cab services, food and beverages, life insurance etc. These can be verified through nature of purchase/expenses in purchase register.

Check Reversal of ITC on excess credit taken due to an error by registered persons on carry forward of CENVAT balances from old regime in TRAN I: check credit taken in TRANS 1 w.r.t last returns filed under old regime. Return compliance in last six months prior to 01.07.2017

Check reversal of ITC on excess credit taken due to an error by a person who was not registered under old regime on stock held on 01.07.2017 in TRANS II: Also verify whether tax credit taken on stock is not older than one year as on 01.07.2017.

Explanation: Expenses should preferably be booked under identifiable heads which enables easy distinction as to applicability of ITC e.g. purchase of insurance should be clearly identifiable in purchase register as life insurance, medical insurance, factory insurance, fire insurance, transit insurance etc. so that easily eligibility of ITC can be verified.

Outward Supply Records:

Outward supply records are also records of tax liability. Outward supply records include:

·Register of Tax Invoices :–– Tax invoices should be serially issued and recorded for domestic supply and export supply containing the following information:

v HSN/SAC Code with item/service name of goods or services supplied

v Invoice No. and date

v GSTIN and name of recipient

v Place of supply

v Type of supply

v applicable GST rate,

v taxable value and tax amount

v status whether reverse charge is applicable

v status whether tax liability is paid though 3B or not

·Register of Bills of Supply; in case of supply of exempted goods or services :–– Bills of supplies should be serially issued and recorded for domestic supply and export supply containing the following information:

v HSN/SAC Code with item/service name of goods or services supplied

v Invoice No. and date

v GSTIN and name of recipient

v Place of supply

v Type of supply

v Exemption status,

v Total value

·Register of Credit Notes and Debit Notes issued serially maintained with reference to original documents against which it was issued

·Register of receipt and refund voucher serially issued and recorded

·Register of goods sent free of cost (FOC) as sample or gift

·Register of goods sent on approval basis on delivery challan

·Register of related party/distinct person supplies

Procedure of Audit of Outward Supply

To conduct GST Audit of outward Supply, an Auditor has to verify whether supply of goods or services are correctly classified as per approved HSN or SAC Code classification list. Verify applicable tax rate according to HSN or SAC Code.

For this, outward supplies need to sorted on HSN or SAC code and verify whether GST Rate has been applied uniformly as prescribed.

Verify invoicing procedure of the registered person. Verify whether correct type of GST is charged with respect to place of supply. Review supplies of exempted goods or services, export of goods or services, or supplies applicable to reverse charge. Verify related party/distinct person transaction and its valuation procedure.

Check valuation of outward supplies as per rule 27 to 35 of GST rule as applicable.

In case where capital goods or plant and machinery of business is sold on which ITC is availed, verify the date of inward supply and the date of outward supply of capital goods to assess liability. Where such capital goods or plant and machinery of business is sold before five years of use, assess liability as follows:

(Total value of ITC / 5years) x No. of years remaining = ITC to be reversed or the tax on the transaction value of such capital goods or plant and machinery determined under section 15, whichever is higher.Verify delivery challan details issued for supply of Semi Knocked Down (SKD) goods, free of cost (FOC) goods, free samples, gifts or branch transfer within state for the same GSTIN.

In case where capital goods or plant and machinery of business is sold on which ITC is availed, verify the date of inward supply and the date of outward supply of capital goods to assess liability. Where such capital goods or plant and machinery of business is sold before five years of use, assess liability as follows:

(Total value of ITC / 5years) x No. of years remaining = ITC to be reversed or the tax on the transaction value of such capital goods or plant and machinery determined under section 15, whichever is higher.Verify delivery challan details issued for supply of Semi Knocked Down (SKD) goods, free of cost (FOC) goods, free samples, gifts or branch transfer within state for the same GSTIN.

Verify non-returnable gate passes - removal of goods for testing, scrap or otherwise (as sample). Verify whether liability of GST is paid on such goods. If liability of GST is not paid, then ITC reversal to be checked on such goods.

Cross verify outward supplies with supplies furnished in GSTR 1 and GSTR 3B to establish any tax liability

Goods Sent on Job work Records:

- Delivery Challan Details for sending and receiving the goods

- Register of rejection /scrap at job workers end

- Register of capital goods sent for Job Work

- Register of Delivery Challan for sending and receiving the Capital goods

- Register of Dies, Moulds, Jigs & Fixtures Provided to Job worker

- Register of rejection /scrap at job workers end

Procedure of Audit of Goods Sent on Job work

To verify details of goods sent on Job Work, an Auditor has to check delivery challan for goods sent on job work.

Verify ITC-04 has been filed regularly every quarter with respect to due dates of every filing or extension thereof

Ensure that pending challans for goods with job worker has not exceeded 360 days for manufacturing goods and 3 years in case of capital goods.

Verify whether stipulated time for return of goods sent on job work has not expired. If stipulated time i.e. 1 year in case of inputs sent to job worker and 3 years in case of capital goods has expired then, list out all such pending challans’ Qty., HSN code, taxable value for computation of liability of GST and interest payable on the same. Interest to be calculated from the date on which goods were initially sent to job worker i.e. the date of delivery challan.

Procedure of Audit of Goods Sent on Approval Basis

For sales subject to customer’s approval. goods must be accepted or returned back within one year.

Verify whether sales subject to customer approval has been supplied on delivery challan. For Audit of such supply, verify such challans and ensure that they are not pending for more than one year. If goods were sent in previous regime then time period shall not be more than 180 days

List out such challans for determining tax liability & interest. Currently interest rate is 18% per annum i.e. 1.5 % per month (the interest has to be calculated from the next day on which tax was due in the month when the goods were dispatched through delivery challan)

Stock Register Records:

This is again very important register from both records and audit perspective

Stock Register Records, If Tax Payer is a Manufacture :

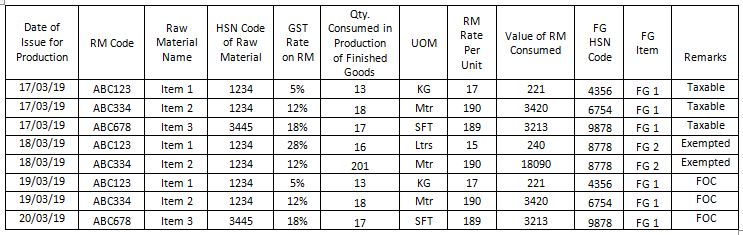

Every registered person manufacturing goods shall maintain periodical records stock register of raw material consumption, consumable consumed, and production showing quantitative details with HSN code, applicable GST Rate and value used in manufacture.

Stock register format of Raw Materials

Opening balance of raw materials and other Inputs

Add: Receipt of Raw Material and other Inputs

Less: Raw Material and other Inputs Consumed in Manufacture or production

Less: Raw Material and other inputs Lost/Stolen/Destroyed/Written off or Disposed

Less: Scrap/By-product and wastage thereof

Closing balance of raw materials and other Inputs goods

Recommended to format for Raw Material Consumption register

Note: Input Tax Credit is not available in case of raw material or inputs lost, destroyed, written off or disposed and needs to be disclosed separately and accounted for.

Every registered person manufacturing goods shall maintain periodical records of input services received showing proportionate value of such service utilized and applied to a product in manufacturing activity i.e. taxable goods production, Exempt goods production and goods supplied as free sample free of cost (FOC) etc.

Input tax credit on input services used in manufacturing of goods are usually common for taxable and exempt goods or otherwise so input services should be applied on individual manufacturing of products on pro-rata basis as mechanism is available in ITC rule.

For example, a machine can produce both taxable and exempt goods so input tax credit on purchase of such machine should be applied on individual product on prorate basis.

Finished goods (production/purchase) stock register format:

Opening Finished Goods

Add: Finished Goods Manufactured During the Month

Less: Finished Goods Lost/Stolen/Destroyed/Written Off or Disposed (No ITC Available on Raw Material Consumed)

Less: Finished Goods Supplied FOC as Sample or gift (No ITC Available on RM Consumed)

Less: Finished Goods Supplied

Closing Finished Goods in Balance

Stock Register in case of Service Provider.

Every registered Service Provider shall maintain accounts details showing details of services utilized and quantitative details of goods used in provision of services.

Stock Register of input goods for provision of service

(Each Service-wise details of input goods in stock to be maintained showing HSN code, GST Rate, Qty and Value.):

Opening Balance of input goods for Provision of Service

Add: Purchase of input goods

Less: input goods Lost/Stolen/Destroyed

Less: Service-wise consumption of input goods

Closing Balance of input goods in hand for provision of Service

Note: No ITC is Available on Input Purchase if such goods are lost stolen or destroyed

Stock Register For Traders

Audit of traders are relatively easier than manufacturer of goods/service provider

Every registered Trader of Goods shall maintain accounts details of each goods traded showing HSN Code, GST Rate, Qty. of Traded Goods with value as Followed:

Opening Balance of Traded Goods

Add: Purchase of Traded Goods

Less: Lost/Stolen/Destroyed/Written Off (No ITC on Purchase)

Less: Traded Goods Supplied FOC for Sample or Gift (No ITC on Purchase)

Less: Traded Goods Sold

Closing Balance of Traded Goods

Procedure of Audit of Stock register

Verify whether all stock register is maintained for each traded goods containing proper HSN code, UOM, Qty. GST Rate, and Value.

Verify whether traded goods supplied free of cost (FOC) for Sample, Gift or lost/stolen/destroyed/written off is maintained separately. Verify reversal of ITC on such goods.

Verify authenticity of disclosures given by registered person for lost/stolen/destroyed/written off of goods.

Related Party/Distinct Person Transaction Record:

Register of Related Parties/distinct person transactions should be maintained separately. Ensure valuation methodology is in accordance with GST valuation rules.

Persons shall be deemed to be related if they fall under any of the categories below:

· An Officer/ director of one business is the officer/ director of another business

· If Businesses are legally recognized as partners

· An employer and an employee

· If Any person holds at least 25% of shares in another company either directly or indirectly

· One of them controls the other directly or indirectly

· They are under common control or management

· The entities together control another entity

· They are members of the same family

Persons shall be deemed to be distinct person if having multiple registration against same PAN number.

Procedure of Audit of Related Party/Distinct Person

Verify related party transactions. Verify whether goods or services are supplied to related party/distinct person as per valuation rules. Verify cost of production or procurement, if goods or services are supplied to related parties/distinct person as per valuation rule 30 cost of production + 10%